Article

There is no shortage of ‘studies’ purporting to bear out the Establishment’s claims in 2016 that Brexit would do great damage to the UK economy. The number of studies and the media coverage accorded to them disguise the inconsistency in the size and nature of the claims: quantity is taken as proof of correctness, whereas content is unconvincing.

The area of consistency in the studies is that the authors consider the EU as a single, homogenous target market for UK exporters, a unitary economic area in which it is inferred that sales opportunities existed but were garnered by suppliers in other EU member states. Absent Brexit, UK suppliers would supposedly have captured these opportunities, raising the UK’s Gross Domestic Product (GDP). In addition, it is taken as read that a substantial amount of value would have been added in the UK, increasing the UK’s wealth, as opposed to the UK’s being used as a pass-through (like Ireland) or as a meeting point between the sales order and imported EU migrant labour, whose costs to the UK economy at best match the value their labour adds.

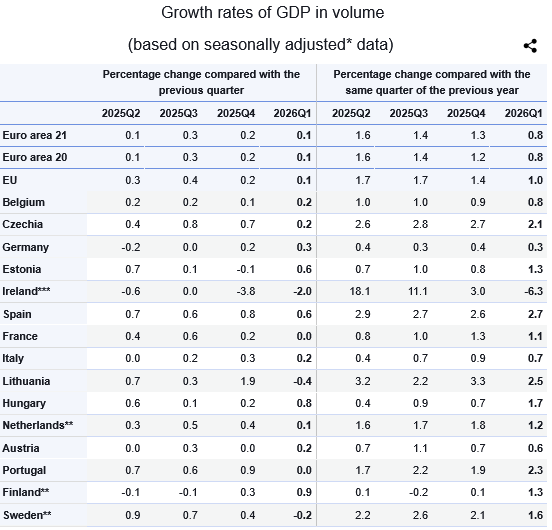

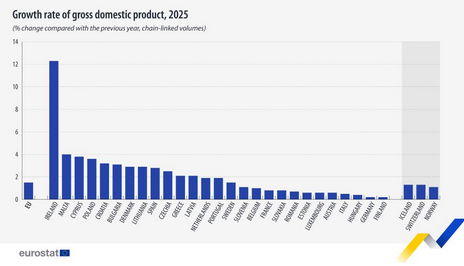

The EU’s own statistics, however, bear no sign that the UK missed out on sales opportunities in the quantity that Rejoiners claim. Indeed the divergence in the economic statistics of EU member states shows that the EU is not a single target market, but 27 different ones, with the Republic of Ireland being a particular outlier. Rejoiner claims fall down in front of realities about the EU Single Market: it has failed to produce the self- sustaining growth that its proponents promised.